Quick Takeaways

- Handwriting OCR converts handwritten estate account books into searchable financial records

- Process executor accounting ledgers, income records, expense tracking, and asset valuations

- Enables verification of estate transactions and preparation of formal accountings

- Critical for probate administration when estate records exist only in handwritten form

- Estate financial records remain confidential throughout processing

Estate account books contain handwritten financial records that executors and administrators maintain during probate administration. These ledgers track income received, expenses paid, asset sales, distributions to beneficiaries, and ongoing management costs. Decades ago, executors kept meticulous handwritten records in bound account books. Even today, some executors maintain handwritten financial tracking alongside or instead of digital records.

These handwritten account books create practical problems for probate administration. You cannot search handwritten ledgers for specific transactions or beneficiaries. You cannot easily verify that all expenses were properly documented. When preparing formal accountings for court approval or beneficiary review, handwritten financial records must be manually transcribed or summarized. If questions arise about estate administration, locating specific transactions in handwritten account books means page-by-page manual review.

This page explains how handwriting OCR makes estate account books searchable and analyzable. It addresses what types of handwritten financial entries it processes, how estate administrators use it for accounting preparation and verification, and realistic expectations when working with historical or contemporary estate financial records.

Why Estate Account Books Matter in Probate

Estate account books document the financial administration of estates. These records provide accountability to beneficiaries, support court filings, and establish that executors properly managed estate assets.

Financial Accountability to Beneficiaries

Executors have fiduciary duties to maintain accurate records of estate financial transactions. Handwritten account books document how estate assets were managed, what income was received, what expenses were paid, and how assets were distributed. These records provide transparency that beneficiaries need to verify proper estate administration.

When account books remain in handwritten form, beneficiaries cannot easily review financial details. They must either accept summary accountings without verification or spend substantial time manually reviewing handwritten ledgers. Questions about specific transactions require locating entries in handwritten records, which is time-consuming and error-prone.

Making estate account books searchable allows beneficiaries to verify transactions, locate specific expenses or distributions, and understand how the estate was administered. This transparency reduces disputes and provides accountability without requiring manual transcription of entire ledgers.

Estate executors maintained handwritten account books documenting every financial transaction, creating detailed records that remain unsearchable until digitized.

Court Accounting Requirements

Probate courts require formal accountings showing estate financial administration. These accountings summarize income, expenses, asset sales, and distributions. Executors must support accounting summaries with detailed transaction records.

When underlying records exist only as handwritten account books, preparing court accountings means manually transcribing or summarizing handwritten entries. Attorneys and accountants spend substantial time converting handwritten ledgers into formal accounting formats. Errors in transcription can create discrepancies that require explanation to the court.

Searchable estate account books accelerate accounting preparation. Financial professionals can locate specific transaction types, verify amounts, and extract data needed for formal accountings without manual transcription. This reduces both preparation time and transcription errors.

Historical Estate Records and Research

Older estates often have only handwritten account books as financial records. When estates remain open for years or when historical research requires understanding estate administration, these handwritten ledgers are the only source of detailed financial information.

Researchers, successor executors, or attorneys investigating historical estate administration need to locate specific transactions or understand financial patterns. Manual review of handwritten account books is time-intensive. Critical information might be missed because handwritten entries cannot be searched.

Digitizing historical estate account books makes them searchable for research, creates preservation copies of deteriorating records, and enables analysis that would be impractical with handwritten-only ledgers.

The Challenge of Handwritten Estate Financial Records

Estate account books combine numerical data, transaction descriptions, dates, and beneficiary names in handwritten form. This creates specific challenges for estate administration and accounting preparation.

Transaction Details Locked in Ledger Format

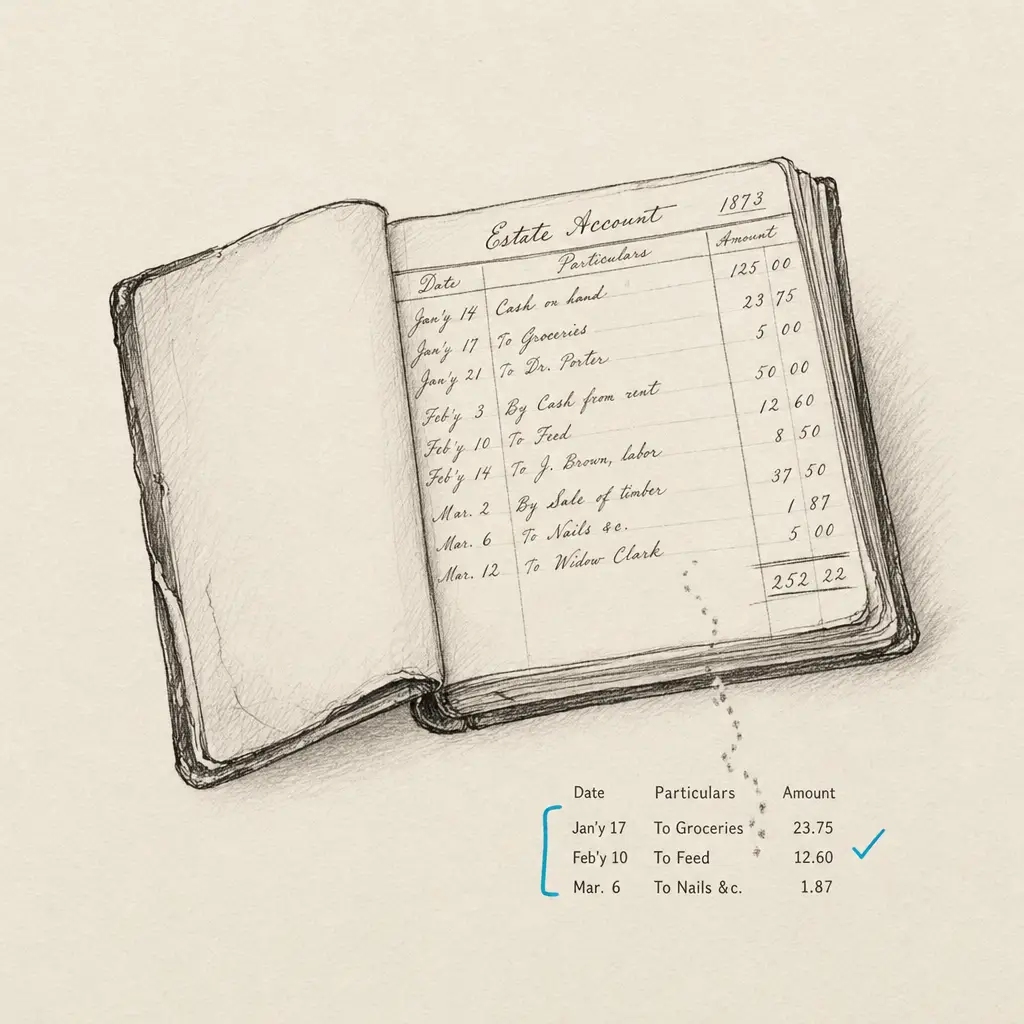

Estate account books typically use ledger formats with columns for dates, descriptions, debits, credits, and running balances. Executors handwrite financial entries in these structured formats. While the structure is clear, the handwritten content is not searchable.

This means you cannot locate all transactions above a certain amount, find all payments to specific vendors, or identify all distributions to particular beneficiaries without manually reviewing every ledger page. Financial analysis that would be straightforward with digital records becomes manual work with handwritten ledgers.

Estate administrators describe spending days manually reviewing handwritten account books to answer specific questions about transactions. During probate administration or beneficiary inquiries, this manual review creates delays and increases administrative costs.

Numerical Accuracy and Verification

Estate accountings must balance. Income plus beginning assets should equal expenses plus distributions plus ending assets. Verifying this requires accurate capture of handwritten numerical entries.

When account books are handwritten, verification means manually checking every numerical entry, recalculating subtotals, and confirming final balances. Handwriting variation in numbers increases transcription error risk. A handwritten “7” might be read as “1” or a “0” as “6.”

This verification challenge means estate accountings based on handwritten records require extra review time to ensure numerical accuracy. Errors discovered late in accounting preparation can require substantial rework.

Verifying handwritten estate account balances requires manual review of every numerical entry, creating risk of transcription errors that delay court filings.

Missing Context Without Searchability

Estate transactions often reference related entries. A distribution entry might note “see expense entry on page 15” or reference an earlier asset sale. Following these cross-references in handwritten account books requires flipping between pages and manually locating referenced entries.

Without searchability, understanding transaction context means manually tracing references through handwritten ledgers. This is time-consuming and risks missing important connections between entries. Financial patterns that would be obvious with searchable records remain hidden in handwritten form.

What Handwriting OCR Processes in Estate Account Books

Handwriting recognition processes the specific types of entries that appear in estate account books. Understanding what it handles helps determine whether it addresses real workflow inefficiencies.

Financial Transaction Entries

Estate account books contain handwritten entries for each financial transaction. These entries typically include transaction dates, descriptions like “sale of real estate” or “attorney fees,” amounts in debit or credit columns, and running balance calculations.

Handwriting OCR processes these transaction entries including dates in various formats, descriptive text that explains transactions, and numerical amounts in currency format. It handles both neat deliberate entries and more rushed handwriting where executors recorded transactions quickly.

This means transaction descriptions become searchable. Estate administrators can locate all attorney fee payments, find distributions to specific beneficiaries, or identify transactions above certain amounts by searching processed account book text.

Numerical Data and Calculations

Account books include handwritten numbers for transaction amounts, subtotals, and running balances. These numerical entries are critical for accounting verification but challenging for OCR because handwritten numbers can be ambiguous.

The technology processes handwritten numerical entries including currency amounts with dollar signs and decimal points, running totals that executors calculated by hand, and date numbers in various formats. It recognizes common number-writing styles while acknowledging that handwritten numerical data requires verification.

Making numbers searchable and extractable enables faster accounting preparation, but numerical accuracy should be verified against original handwritten entries for financial records where precision matters.

Beneficiary and Vendor Names

Estate account books include handwritten names of beneficiaries receiving distributions, vendors paid for services, and financial institutions managing estate accounts. These names appear repeatedly throughout account books.

Handwriting OCR processes proper names including beneficiary names in various handwriting styles, vendor business names, and financial institution names. It handles name variations where executors abbreviated or spelled names differently across entries.

Searchable names allow estate administrators to locate all transactions involving specific beneficiaries or vendors. This is valuable for answering questions about distributions or documenting payments to particular service providers.

| Record Type | Typical Content | Common Challenges | Searchability Benefit |

|---|---|---|---|

| Income entries | ”Rent received,” “dividend payment,” amounts | Abbreviated sources, variable formats | Locate all income by type or source |

| Expense records | ”Attorney fees,” “property maintenance,” amounts | Handwritten vendor names, unclear descriptions | Find all expenses of specific types |

| Distribution entries | Beneficiary names, amounts distributed, dates | Name variations, partial distributions | Track all distributions to each beneficiary |

| Asset transactions | ”Sale of stock,” valuations, proceeds | Complex transaction descriptions | Locate asset sales and valuations |

| Running balances | Calculated totals, account balances | Handwritten calculation errors | Verify accounting mathematics |

How Estate Administrators Use Account Book OCR

Making estate account books searchable addresses specific bottlenecks in probate administration and accounting preparation. Estate professionals apply this capability to formal accounting preparation, beneficiary inquiries, and financial verification.

Formal Accounting Preparation

Probate attorneys and accountants preparing formal estate accountings need to summarize transactions from estate records. When those records are handwritten account books, preparation means manually extracting and categorizing transactions.

With searchable account books, professionals can locate all transactions of specific types, extract amounts for specific categories, and verify totals without manual transcription. They search for all “attorney fees” entries to summarize legal costs, find all distributions to calculate total amounts distributed, or locate asset sales to document proceeds.

Estate professionals describe substantial time savings when preparing accountings from searchable rather than handwritten-only records. What might take days of manual transcription becomes hours of searching and verification.

For broader context on estate handwriting, see the parent guide on probate and estate handwriting OCR.

Searchable estate account books reduce formal accounting preparation time from days of manual transcription to hours of targeted data extraction.

Beneficiary Inquiry Response

Beneficiaries ask questions about estate administration. They want to know what attorney fees were paid, when distributions were made, or how specific assets were handled. Answering these questions from handwritten account books requires manual review.

With searchable account books, executors or estate attorneys can quickly locate relevant transactions to answer beneficiary questions. They search for the beneficiary’s name to find all distributions, look up specific expense types to explain costs, or locate asset transactions to document handling.

This responsiveness reduces beneficiary concerns and disputes. Questions can be answered promptly with specific transaction references rather than requiring extensive manual review before responding.

Financial Verification and Auditing

Estate accountings must balance and transactions must be properly documented. Verification involves checking that income entries match bank deposits, expenses are supported by receipts, and distributions equal amounts authorized.

Searchable account books enable targeted verification. Auditors can locate all entries above certain amounts for detailed review, find transactions on specific dates to match against bank records, or identify beneficiaries receiving distributions to verify authorizations.

This makes verification more efficient and thorough. Rather than sampling transactions because comprehensive review is impractical, auditors can search for specific transaction types or patterns that warrant examination.

Historical Estate Research

Attorneys handling old estates or legal disputes about historical estate administration need to understand how estates were managed years or decades ago. Handwritten account books from these estates contain the detailed financial information needed.

Searchable historical account books allow researchers to locate specific transactions, trace asset handling over time, or understand financial patterns without manually reviewing entire ledgers. This supports legal research, historical analysis, or resolution of estate disputes.

Realistic Expectations for Estate Account Books

Estate account books vary in handwriting quality, numerical clarity, and record-keeping consistency. Understanding what handwriting OCR handles well and what requires verification helps set appropriate expectations.

What Works Well

Structured ledger formats with consistent entry types work effectively. When executors maintained organized account books with standard columns and predictable entry formats, OCR processing produces reliable results.

Clear handwriting from executors who wrote carefully produces accurate text conversion. Professional executors or those with accounting backgrounds often maintained neat records that support effective OCR processing.

Standard financial terminology and common transaction descriptions are recognized reliably. Terms like “attorney fees,” “real estate taxes,” or “distribution to beneficiary” appear frequently and are processed consistently.

What Requires Verification

Handwritten numerical data needs verification for financial accuracy. While OCR can process numbers, the critical nature of financial data means amounts should be spot-checked against original handwritten entries, especially for large transactions or final balances.

Personal abbreviations and informal record-keeping require interpretation. Some executors developed personal shorthand or abbreviated transaction descriptions. While the handwriting can be converted to text, understanding what abbreviations mean may require context.

Faded or deteriorated historical account books present image quality challenges. Very old ledgers might have ink fading, water damage, or page deterioration. These materials still benefit from digitization before further deterioration, but output quality depends on source legibility.

Maintaining Financial Accuracy

Estate account books are financial records where accuracy matters for legal compliance and beneficiary accountability. Handwriting OCR makes these records searchable and accelerates accounting preparation, but it does not replace the need for financial verification.

Transaction amounts, especially large values and final balances, should be verified against handwritten originals. The goal is making account books searchable while maintaining the financial accuracy required for probate administration and court filings.

Professional judgment about when to verify specific entries against handwritten sources remains important. The technology provides searchability and extraction capabilities, but estate professionals determine appropriate verification procedures for their circumstances.

Privacy and Estate Record Confidentiality

Estate account books contain confidential financial information about deceased persons and their beneficiaries. These records include asset values, beneficiary identities, and detailed financial transactions that must be protected.

How Record Confidentiality Works

When you process estate account books through handwriting OCR, records are handled only to deliver results to you. They are not used to train AI models. They are not retained longer than necessary for processing. They are not shared with third parties or made accessible to other users.

This matters for estate records that contain sensitive financial information and personal data about beneficiaries. Professional responsibilities and privacy laws require confidential handling of estate financial records. The service maintains these protections throughout processing.

Your estate account books remain under your control. You upload handwritten records, receive searchable text output, and maintain custody of both originals and processed results. The service does not claim rights to estate records or access them for purposes other than OCR processing.

Professional Responsibility for Estate Records

Attorneys, accountants, and executors have professional and fiduciary obligations regarding estate record confidentiality. Using OCR services to digitize and process estate account books does not eliminate these obligations.

The service provides infrastructure to handle estate records confidentially, but professionals make determinations about appropriate use under applicable ethical rules, privacy laws, and fiduciary duties. Estate records remain subject to the same confidentiality requirements whether in handwritten or digitized form.

Security for Financial Records

Estate account books are transmitted and processed using security protocols appropriate for confidential financial records. Documents are encrypted during transmission. Processing occurs in secure environments with access limited to systems necessary for OCR operations.

This infrastructure recognizes that estate financial records contain sensitive information requiring appropriate security. While no technology eliminates all risk, the architecture prioritizes security suitable for professional use with confidential estate materials.

Getting Started with Estate Account Books

If you are dealing with handwritten estate account books and need to make them searchable for accounting preparation or beneficiary inquiries, the most direct approach is testing with your actual estate records.

Estate record-keeping varies by executor, time period, and estate complexity. Some executors maintained meticulous structured ledgers while others kept informal handwritten notes. The only way to know whether handwriting OCR will improve your specific workflow is testing it on the types of estate account books you actually work with.

HandwritingOCR offers a free trial with credits for processing sample documents. Upload pages from estate account books with handwritten transaction entries, numerical records, or beneficiary information. See how the searchable output compares to manual transcription or data extraction.

Your estate records remain confidential throughout testing. Documents are processed only to deliver results to you and are not used for any other purpose. This allows estate professionals to test functionality without compromising fiduciary obligations regarding confidential estate information.

The service is straightforward to use. Upload scanned estate account book pages, process them, and download searchable text output. There is no complex setup, no software installation, and no commitment required to determine whether it works for your materials.

If it reduces time spent manually transcribing estate transactions or locating specific entries for accounting preparation, it likely delivers similar benefits on comparable materials. If numerical accuracy or handwriting recognition does not meet your requirements, you have learned that before investing further. Either way, you will understand whether handwriting OCR addresses practical bottlenecks in your estate administration workflows.

For additional context on processing other types of estate handwritten materials, see guides on handwritten wills, handwritten estate inventories, and handwritten executor correspondence. The broader context for estate handwriting appears in our guide to probate and estate handwriting OCR.

Frequently asked questions

Can handwriting OCR process the numerical entries in estate account books accurately?

Yes, handwriting OCR processes handwritten numbers in estate account books including transaction amounts, running balances, and calculated totals. However, because financial accuracy is critical for estate accountings, numerical entries should be verified against original handwritten records, especially for large transactions and final balances. The technology makes numbers searchable and extractable, but professional verification ensures financial precision required for probate administration.

How does searchable estate account book help with formal accounting preparation?

Searchable account books allow attorneys and accountants to locate all transactions of specific types without manual transcription. They can search for all attorney fees to summarize legal costs, find distributions to calculate total amounts paid to beneficiaries, or locate asset sales to document proceeds. This reduces formal accounting preparation from days of manual work to hours of targeted extraction and verification.

Are estate account books kept confidential when processed through handwriting OCR?

Yes, estate account books are processed only to deliver results to you and are not used to train AI models, shared with third parties, or retained longer than necessary. This protects confidential financial information about estates and beneficiaries. Estate professionals can process account books while maintaining compliance with fiduciary duties and professional obligations regarding estate record confidentiality.

Can handwriting OCR handle old estate account books from decades ago?

Yes, the technology processes historical estate account books including older handwriting styles and ledger formats used in past decades. However, very old account books may have image quality challenges from faded ink, water damage, or page deterioration. These materials still benefit from digitization to create preservation copies before further deterioration, though output quality depends on source document legibility.

What file formats work for processing estate account book pages?

Handwriting OCR processes scanned PDFs and image formats including JPG, PNG, and TIFF. Estate account books are typically scanned as multi-page PDFs or photographed as images, both of which work directly without conversion. The output is delivered as searchable text in formats like Word (DOCX), plain text, or Excel for financial data extraction depending on workflow needs. There is no special preparation required beyond having scanned images of account book pages.